The Best Business Valuation Guide 2026: DCF, Relative Valuation, SOTP & Holding Company Methods Explained

Dr. Gaurav B.

Founder & Principal Valuer, Transaction Capital LLC

Specialist in IRS-Compliant 409A & Complex Valuation Matters

Dr. Gaurav B. is the Founder and Principal Valuer of Transaction Capital LLC, a valuation and financial advisory firm providing independent, standards-based valuation opinions for startups, growth-stage companies, and established enterprises.

A business valuation guide helps founders, CFOs, investors, and attorneys determine what a company is truly worth. Whether you need a valuation for fundraising, M&A, tax compliance, or litigation, understanding the right methodology can mean the difference between leaving millions on the table and making a well-informed decision.

In 2026, accurate business valuation matters more than ever. Regulatory scrutiny from the IRS and SEC is intensifying. AI-driven tools are reshaping how analysts build financial models. And the looming TCJA estate tax sunset is creating urgency for wealth transfer planning.

At Transaction Capital LLC, our ABV®, ASA, CVA®, and MRICS certified professionals have completed 2,500+ valuations across 35+ industries. We combine deep technical expertise with fast turnaround and transparent pricing.

This guide walks you through every major valuation method, explains when to use each one, and provides real-world examples to help you navigate even complex scenarios.

Need Expert Guidance?

Schedule a free 15-minute consultation with our certified appraisers to discuss your valuation needs and get personalized insights.

Schedule Your Free ConsultationWhat Determines a Company’s or Business Value?

A company’s value is shaped by both internal fundamentals and external market conditions. No two businesses are alike, so no single formula applies universally. Here are the factors that professional appraisers evaluate:

- Purpose of Valuation: Valuation objectives include fundraising, 409A compliance, litigation, M&A, and financial reporting.

- Business stage: early-stage startup, scaling business, or mature organization

- Financial health: revenue model, profitability, capital structure, and liabilities

- Intangible drivers include brand equity, IP portfolio, leadership quality, and customer loyalty.

- Industry and Macro Trends: Industry and macro trends include regulatory changes, competitive intensity, and economic cycles.

External influences include industry dynamics, competitive intensity, regulatory changes, interest rate environments, and macroeconomic cycles.

In 2026, factors like elevated interest rates, tighter IRS enforcement on stock option compliance, and the impending estate tax exemption reduction are directly affecting how businesses are valued.

What Standard and Premise Value Should You Use?

Before selecting a valuation approach, it is essential to define two foundational concepts:

1. Standard Value specifies the type of value being measured. The three most common standards are fair market value (FMV) – the price a willing buyer and seller would agree on, each acting without pressure – investment value (value to a specific buyer considering synergies), and liquidation value (proceeds from an orderly or forced asset sale).

2. Premise of Value describes the assumed conditions of the sale. A going concern premise assumes the business will continue operating. An orderly liquidation assumes assets are sold over a reasonable time frame. A forced sale assumes assets must be sold quickly, typically at a discount.

Key Takeaway: Price is what you pay. Value reflects what something is genuinely worth to you. Valuation is always contextual – the purpose, the audience, and the market conditions all shape the final number.

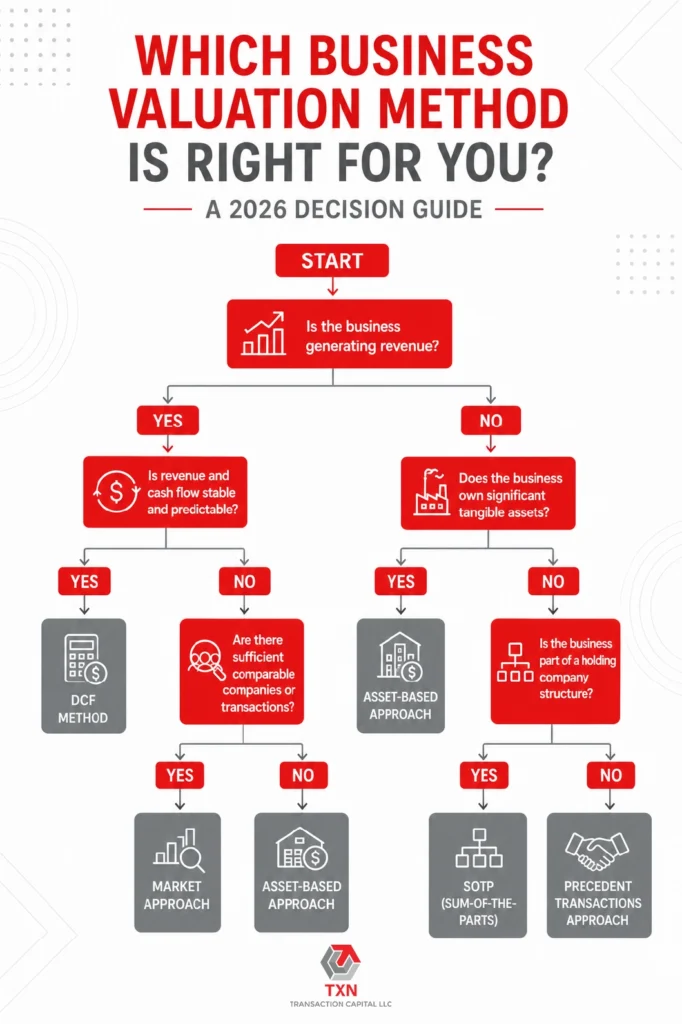

How Do You Choose the Right Business Valuation Method?

Selecting the appropriate methodology depends on the company’s characteristics, the purpose of the valuation, and the available data. Professional appraisers rarely rely on a single method. Instead, they triangulate results from multiple approaches to arrive at a defensible range.

Here is a decision framework:

|

Method |

Best Suited For |

Key Requirement |

|

DCF (Discounted Cash Flow) |

Revenue-generating companies with projectable cash flows |

Reliable financial forecasts |

|

Relative Valuation (Market Approach) |

Companies with comparable public peers or recent transactions |

Sufficient comparable data |

|

Asset-Based |

Asset-heavy businesses, holding companies, or distressed firms |

Fair value balance sheet |

|

SOTP (Sum of the Parts) |

Diversified conglomerates or multi-segment companies |

Segmented financial data |

|

Holding Company |

Investment holding entities with passive asset portfolios |

Clear asset inventory |

For instance, a SaaS company might anchor a DCF model, cross-check with revenue multiples from comparable transactions, and then apply appropriate discounts for illiquidity.

Core Components of a DCF Model

The discounted cash flow (DCF) method is widely regarded as the gold standard for intrinsic business valuation. It calculates what a business is worth today based on the cash it is expected to generate in the future. The core logic rests on the time value of money: a dollar earned today is worth more than a dollar earned next year because it can be invested immediately.

1. Forecast Free Cash Flow?

Free Cash Flow (FCF) represents the cash available to all capital providers after reinvesting in the business. The formula is:

FCF = EBIT − Taxes + Depreciation − Capital Expenditure − Change in Working Capital

Forecasts typically span 5 to 10 years and incorporate revenue projections by segment, gross margin stability, SG&A trends, CapEx requirements, and reinvestment strategy.

In our valuation practice, we build multiple scenarios (base, optimistic, conservative) weighted by probability using the Probability Weighted Expected Return Method (PWERM) – particularly useful for venture-backed companies with uncertain trajectories.

2. Terminal Value Calculated

Terminal value captures all cash flows beyond the explicit forecast period. Because businesses are assumed to operate indefinitely, this figure often represents 60–80% of total enterprise value – making it the single most important assumption in a DCF model.

Two methods dominate:

The Gordon Growth Model assumes the business generates free cash flow that grows at a constant rate into perpetuity. A typical long-term growth rate of 2–3% approximately GDP plus inflation expectations. The formula is: Terminal Value = Final Year FCF × (1 + g) / (WACC − g).

The Exit Multiple Method applies an EV/EBITDA or EV/Revenue multiple to the final forecast year’s earnings. This approach anchors terminal value to observable market data. In 2026, most practitioners cross-check both methods to identify valuation bias.

3. Discount Rate – WACC (Weighted Average Cost of Capital)

The Weighted Average Cost of Capital (WACC) serves as the discount rate. It reflects the blended return required by all capital providers – equity and debt.

The cost of equity is typically derived using the Capital Asset Pricing Model (CAPM), which incorporates the risk-free rate (the 10-year US Treasury yield was approximately 4.2% in early 2026), equity risk premium, company-specific beta, and a size premium for smaller firms.

The cost of debt is calculated after adjusting for the effective tax rate (the federal corporate rate remains 21% in 2026).

Additional adjustments may include company-specific risk premiums (CSRP) for factors like customer concentration, key-person dependency, or regulatory exposure; illiquidity premiums for private companies; and country risk premiums for cross-border operations.

For reference, WACC ranges typically fall between 8–10% for large-cap companies and 12–20% for startups and small-cap firms.

4. Calculate Present Value

Once FCFs and terminal value are projected, each cash flow is discounted back to today using WACC:

Enterprise Value (EV) = Present Value of FCFs + Present Value of Terminal Value

Equity Value = Enterprise Value − Net Debt + Excess Cash

This “EV-to-equity bridge” is where many online valuation guides stop short. In real transactions, the definitions of net debt and working capital directly affect what sellers receive at closing.

At Transaction Capital LLC, we document every bridge adjustment to ensure our reports are audit-defensible and transparent.

What Are Common Challenges in DCF Valuation?

DCF models are powerful but sensitive to assumptions. Small changes in the discount rate or growth rate can shift the result by 20–30%.

Common pitfalls include over-optimistic revenue projections, using generic WACC estimates instead of company-specific rates, and letting terminal value dominate the total without sanity-checking the implied exit multiple.

At Transaction Capital LLC, we address these challenges by modelling scenarios using PWERM to capture a range of outcomes, utilizing Duff & Phelps (now Kroll) and Ibbotson data for accurate cost of capital calculations, developing tailored terminal value methodologies for tech, SaaS, and cyclical businesses, documenting all assumptions and inputs for audit purposes, and applying valuation waterfall modelling to manage capital stack complexity.

How Does Relative Valuation Work?

Relative valuation, also called the market approach, compares your business to similar public or private companies using valuation multiples. This method answers a straightforward question: “How are comparable businesses priced in today’s market?”

Key Multiples Used

The most applied multiples include:

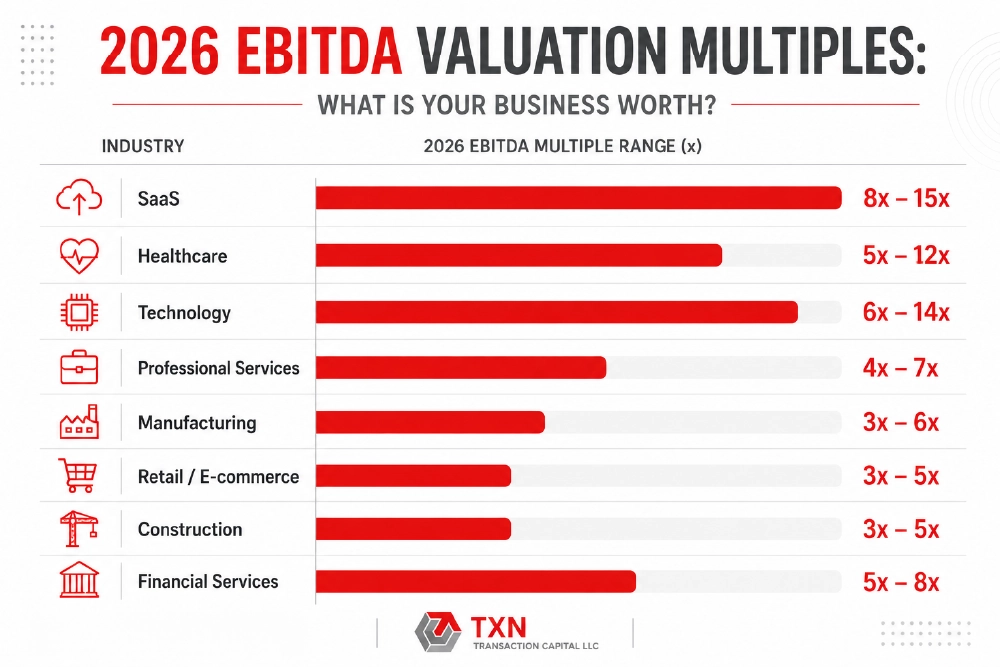

EV/EBITDA is the workhorse of M&A and private equity transactions. It strips out capital structure differences and is particularly useful for comparing companies with different debt levels. In 2026, median EV/EBITDA multiples for US private companies range from 3x–6x for traditional SMBs, 4x–8x for mid-market firms, and 8x–15x+ for high-growth technology companies.

1. Price/Earnings (P/E) Ratio is common for mature, profitable enterprises where earnings are stable and predictable.

2. EV/Revenue is ideal for early-stage and SaaS companies that may not yet be profitable but demonstrate strong recurring revenue growth. SaaS companies with net revenue retention above 120% commonly trade at 5x–10x forward revenue.

3. Price-to-Book (P/BV) is important for financial institutions and asset-heavy businesses where tangible asset values closely reflect market value.

Why Use Relative Valuation?

This approach offers effective market communication and relevance, faster execution than DCF without the need for long-term forecasts, and is ideal for fundraising, IPOs, M&A benchmarking, and 409A valuation support.

What Are the Limitations?

Relative valuation depends on selecting an appropriate peer group. It also compresses risk, growth, and capital structure into a single metric. Peer companies may differ in stage, geography, or accounting standards, potentially producing misleading comparisons. Published multiples often lag actual market conditions by 6–12 months and can be inflated by earn-outs or deferred payment structures.

How Does Transaction Capital Improve Relative Valuation?

1. Intelligent Peer Selection. We use filters beyond SIC/NAICS codes to match customer segments, pricing strategies, capital intensity, growth trajectory, and geographic and regulatory exposure.

2. Forward Multiples for Future Projections. This is especially important for SaaS and technology companies. Instead of relying on historical data, we apply EV/EBITDA multiples based on 2026–2027 consensus estimates.

3. Valuation Adjustments. We normalize one-time costs and gains, adjust for non-operating assets such as surplus cash, and account for intangibles including intellectual property, technology stack, and brand equity.

4. Global Comps with Regional Adjustments. When local peers are unavailable, we adjust global comparables for currency fluctuations, country-specific tax regimes, inflation, and capital market maturity.

5. Certified Standards. All reports comply with ABV® (AICPA), ASA® (American Society of Appraisers), CVA® (NACVA), and meet IRS 409A, ASC 718, IVS, and USPAP requirements.

What Is an Asset-Based Valuation?

The asset-based approach calculates business value by determining the fair market value of all assets, tangible and intangible, and subtracting liabilities. The formula is simple:

Business Value = Total Assets (at Fair Value) − Total Liabilities

This method works best for asset-heavy sectors like manufacturing, real estate, and transportation, or for businesses with inconsistent profitability. It also serves as a “floor valuation” – representing what a company would be worth if liquidated for parts rather than sold as a going concern.

However, the approach has limitations. It often undervalues goodwill, brand strength, customer relationships, and other intangible assets that may represent the majority of a company’s true worth. Balance sheet figures based on historical cost accounting rarely reflect current market values.

For these reasons, professional appraisers typically use the asset-based approach alongside income or market methods rather than standalone valuation.

What Is the Sum of the Parts (SOTP) Valuation?

SOTP valuation is best suited for diversified organizations with multiple divisions, subsidiaries, or investment interests. Rather than applying a single multiple to the entire company, this method assigns independent values to each segment and then aggregates them.

When Should You Use SOTP?

Common use cases include conglomerates with unrelated business lines, private equity portfolios or special purpose vehicles with multiple assets, companies with both high-growth and mature divisions, and restructuring scenarios where individual divisions may be sold separately.

How Does SOTP Work?

The process follows four steps:

Step 1: Identify distinct business segments based on different industries, geographies, or revenue models.

Step 2: Value each division individually using the most appropriate method – DCF for segments with predictable cash flows, comparable company analysis for those with strong public peers, or net asset value for asset-intensive segments.

Step 3: Sum all segment values to arrive at the total enterprise value.

Step 4: Apply a conglomerate discount (typically 10–30%) to account for management overhead, reduced transparency, and lack of strategic cohesion. Then subtract net debt to arrive at equity value.

SOTP Worked Example

Consider a diversified technology company with three segments:

|

Segment |

EBITDA |

Multiple |

Implied EV |

|

Cloud Services |

$5M |

12x |

$60M |

|

IT Consulting |

$3M |

6x |

$18M |

|

Hardware Distribution |

$2M |

4x |

$8M |

|

Subtotal |

$86M | ||

|

Conglomerate Discount (15%) |

−$12.9M | ||

|

Adjusted Enterprise Value |

$73.1M |

This segmented approach reveals that the cloud services division drives 70% of the company’s total value insight that would be obscured by a blended company-wide multiple.

How Do You Value a Holding Company?

Holding companies frequently report little to no operating income. Their value is derived from the underlying assets they own, not from the revenue they generate directly.

The valuation process involves identifying and independently valuing each asset class: listed equity positions (valued at current market price or DCF), private equity holdings (DCF or relative value with appropriate discounts), and real estate, intellectual property, and alternative investments (appraised at fair market value).

Key Considerations for Holding Company Valuations

Minority interest discounts apply when the holding company owns less than a controlling stake. Illiquidity discounts are relevant for unlisted or thinly traded investments.

Tax implications for potential asset disposal must be factored in, as a holding company that would incur significant capital gains taxes upon selling an asset may be worth less than the sum of its gross asset values.

Transaction Capital use a bottom-up approach, evaluating each asset class independently and applying the required control, liquidity, and tax-related adjustments. This methodology ensures that the final valuation reflects real-world conditions rather than theoretical maximums.

What Do Business Buyers Actually Pay For?

Understanding buyer psychology is essential for anyone seeking a valuation – whether for sale, fundraising, or strategic planning. Buyers are not purchasing your company’s past; they are paying certainty about its future.

Four factors determine how much a buyer will pay:

1. Profit quality is the foundation. Buyers care about sustainable, repeatable earnings — not one-off spikes. A company generating $500K in consistent EBITDA over three years is far more valuable than one showing $700K with peaks, troughs, and customer dependencies.

2. Growth trajectory is the multiplier. Credible, achievable growth that doesn’t rely on a single individual or lucky breaks commands premium multiples. Documented pipeline, proven scalability, and IP-protected products with all signal upsides.

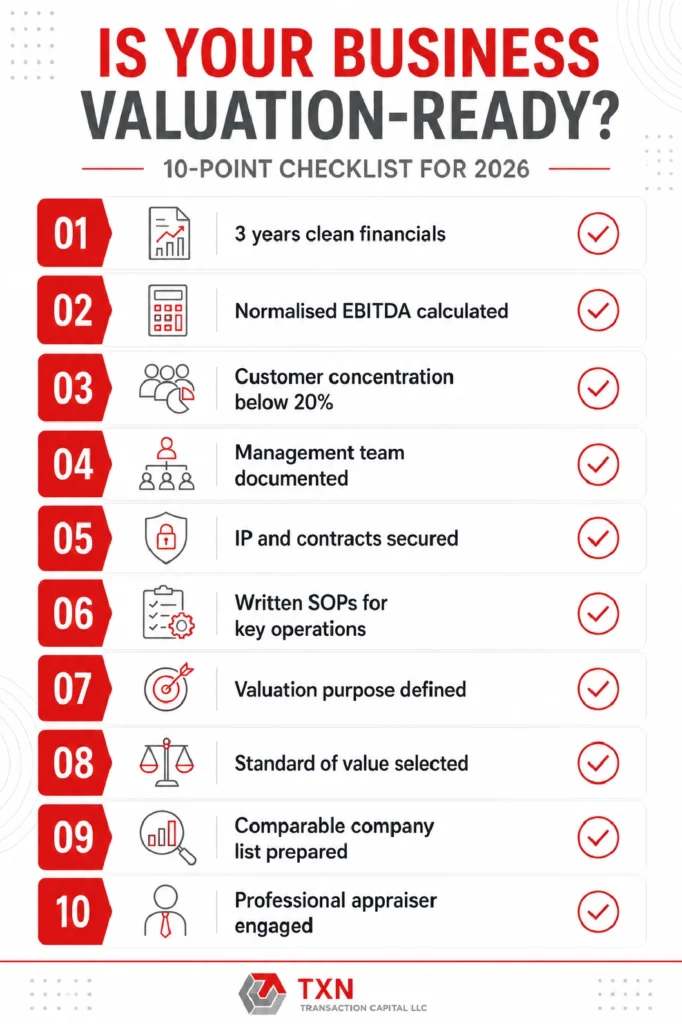

3. Risk profile is the silent valuation killer. Customer concentration (any single client above 20% of revenue), founder dependency, weak financial systems, and key-person reliance each reduce the multiple a buyer is willing to pay.

4. Transferability is the ultimate test. Can the business perform the same after the sale as it did before? A capable management team, documented processes, and diversified customer relationships managed by the team, not the owner signal that the business can run independently.

Based on our valuation practice, two companies with identical earnings can have valuations that differ by 50% or more based solely on these qualitative factors.

How Can You Increase Your Business Value Before Valuation?

Valuation is not a fixed number; it is a snapshot that can be deliberately improved. Here are actionable steps most business owners can implement within 12–24 months:

1. Strengthen profit quality. Focus on recurring revenue streams. Review pricing by product line and trim unprofitable revenue. At typical multiples, every $10,000 of verified recurring profit adds $40,000–$60,000 to enterprise value.

2. Build management of independence. Delegate authority. Appoint or upskill a general manager. Create written procedures for key operations. If you can take a two-week vacation without business stalling, you have already improved your sale price.

3. Diversify your customer base. No single customer should represent more than 15–20% of revenue. Convert informal arrangements into written contracts.

4. Document everything. Buyers value order and reliability. Clean management accounts, documented SOPs, and a well-organised data room for signal professionalism and reduce due-diligence friction.

5. Get a valuation early. A valuation is not a sale trigger; it is a planning tool. Understanding your current value drivers helps you identify what to fix before going to market.

What Are Common Business Valuation Mistakes to Avoid?

In our experience working with startups and established enterprises, several recurring errors can undermine a valuation’s credibility and expose companies to regulatory risk:

1. Using unadjusted accounting profits. Reported earnings often include personal expenses, one-off items, or non-market-rate owner compensation. Professional valuations normalize these to reflect true maintainable earnings.

2. Selecting inappropriate comparable companies. Comparing a 20-person SaaS startup to a $1 billion public company without adjusting for size, stage, and risk produces unreliable results.

3. Ignoring the EV-to-equity bridge. A company may have an enterprise value of $10 million, but if it carries $3 million in debt, the equity value is only $7 million. Many DIY valuations overlook this critical step.

4. Relying on a single method. Professional standards (USPAP, SSVS, IRS Revenue Ruling 59-60) all recommend triangulating results from multiple approaches.

5. Using automated “black box” platforms. Algorithmic valuations often fail to account for complex capital structures, idiosyncratic risks, or off-balance-sheet items. In 2026, the IRS is increasingly scrutinizing low-cost, software-generated 409A reports that lack documented assumptions and expert sign-off.

What Does a Professional Business Valuation Cost in 2026?

Valuation costs vary significantly depending on complexity, purpose, and provider. Here is a general pricing framework:

|

Provider Type |

Typical Cost |

Turnaround |

Best For |

|

Online calculators |

Free–$200 |

Instant |

Rough estimates only |

|

SaaS platforms |

$500–$2,000 |

1–3 days |

Simple startups |

|

Boutique firms (like TXN Capital) |

$500–$5,000+ |

2–5 business days |

Audit-ready, defensible reports |

|

Big 4 accounting firms |

$15,000–$50,000+ |

4–8 weeks |

Large enterprises, IPOs |

Transaction Capital LLC offers professional, audit-defensible valuations starting at $500 with delivery in 2–5 business days. Our “Pay After Draft Review” policy means you review the preliminary findings before committing financially, a risk-reversal model designed to give you confidence in the process.

How Do 2026 Market Trends Affect Business Valuations?

Several forces are shaping the valuation landscape this year:

1. Interest rates and capital costs remain elevated compared to the near-zero environment of 2020–2021. Higher discount rates compress DCF valuations, and leveraged buyout appetite has softened. Cash-rich buyers and strategic acquirers now dominate M&A activity.

2. AI integration is reshaping both how valuations are performed and what is valued. Companies with proprietary AI models, curated datasets, and scalable AI infrastructure command premiums. At the same time, AI is enabling faster data extraction and comparable analysis, improving efficiency for valuation firms.

3. The TCJA estate tax sunset is creating urgency. The current $13.6 million per-person federal estate tax exemption is set to be roughly halved in 2026. High-net-worth individuals are accelerating gift and estate tax valuations to maximise wealth transfer before the deadline.

4. IRS enforcement is tightening. The agency is devoting more resources to auditing stock-based compensation and private company valuations. Reports lacking documented assumptions, proper methodology, or expert credentials face increased scrutiny.

5. ESG-integrated valuations are becoming a requirement for impact investors and institutional LPs, adding a new dimension to portfolio and company-level assessments.

Ready to get started?

Request your valuation quote today and review the draft before you pay.

Request Your Quote →Final Thoughts: Why Transaction Capital LLC Stands Apart

Transaction Capital LLC provides more than valuation reports – we deliver strategic clarity. Our clients include venture-funded startups, global corporations, family offices, and institutional investors who need valuations that are defensible under audit, admissible in court, and trusted by investors.

Our services extend beyond compliance. We identify value drivers, flag operational inefficiencies, and recommend capital optimization strategies that help you make better strategic decisions.

Take the next step. Contact Transaction Capital LLC for a compliant, audit-defensible valuation backed by 2,500+ engagements across 35+ industries.

Frequently Asked Questions

1. What is the most accurate method for valuing a business?

No single method is universally “most accurate.” Professional appraisers typically combine DCF analysis with relative valuation and asset-based approaches to triangulate a defensible range. The best method depends on the company’s stage, industry, available data, and the purpose of the valuation.

2. How much does a professional business valuation cost in 2026?

Costs range widely from free online calculators to $50,000+ from Big 4 firms. Transaction Capital LLC offers audit-ready valuations starting at $500 with delivery in 2–5 business days, making professional-grade reports accessible to startups and mid-market companies alike.

3. What is the difference between enterprise value and equity value?

Enterprise value represents the total value of a company’s operations, including both debt and equity. Equity value is what remains for shareholders after subtracting net debt and adding excess cash. In M&A transactions, deals are typically negotiated on an enterprise value basis, then adjusted to equity value at closing.

4. When should a business get a professional valuation?

Key trigger events include fundraising rounds, issuing stock options (409A compliance), M&A transactions, estate and gift tax planning, litigation or divorce proceedings, annual goodwill impairment testing, and ESOP formation. Getting a valuation 12–18 months before a planned exit allows time to address weaknesses and improve value.

5. What EBITDA multiple can I expect for my business in 2026?

EBITDA multiples vary significantly by industry, size, and risk profile. Traditional SMBs typically trade at 3x–6x EBITDA, mid-market companies at 4x–8x, and high-growth technology firms at 8x–15x or higher. Customer concentration, founder dependency, and recurring revenue quality all influence where your business falls within the range.

6. How does the 2026 TCJA estate tax sunset affect business valuations?

The Tax Cuts and Jobs Act exemption is scheduled to be approximately halved in 2026. This means high-net-worth individuals should accelerate wealth transfer strategies now, while higher exemption still applies. Professional gift and estate tax valuations with appropriate discounts for lack of control and marketability can reduce taxable values by 20–40%.

7. Can an automated tool replace a professional business valuation?

Automated tools provide rough estimates but typically cannot account for complex capital structures, idiosyncratic business risks, or nuanced regulatory requirements. For 409A compliance, audit defense, litigation, or M&A, an independent valuation signed by credentialed professionals (ABV®, ASA, CVA®) is strongly recommended and may be legally required.

8. What makes a valuation audit-defensible?

An audit-defensible valuation documents all assumptions, applies recognized methodologies (DCF, market approach, asset-based), complies with professional standards (USPAP, SSVS, IVS), and is signed by a credentialed appraiser. Transaction Capital’s reports are designed to withstand scrutiny from Big 4 auditors, the IRS, and courts.