How to Calculate Seller’s Discretionary Earnings (SDE): A 2026 Guide for Small Business Owners

Introduction

Seller’s Discretionary Earnings (SDE) represents the total financial benefit a single, full-time owner-operator derives from a business on an annual basis.

It is the most widely used metric for valuing owner-operated companies generating less than $5 million in annual revenue, and it forms the foundation of virtually every Main Street business sale, SBA loan application, and acquisition negotiation in the United States.

If you are a small or mid-sized business owner, “What is my business actually worth?” – the answer almost always starts with your SDE. Not your revenue. Not your net income. Not even your EBITDA. Those metrics tell part of the story.

SDE tells the whole story by stripping away financing choices, personal spending habits, and one-time anomalies to reveal exactly how much money a new owner-operator could reasonably take home each year.

Whether you are preparing to sell in the next 12–36 months, applying for an SBA 7(a) loan, defending your valuation in a partnership dispute, or simply benchmarking your performance against the industry, understanding how to calculate seller’s discretionary earnings accurately is essential.

At Transaction Capital LLC, our ABV®, ASA, CVA®, and MRICS certified professionals have completed over 2,500 valuations across 35+ industries—and SDE analysis sits at the core of nearly every small business engagement we handle.

Key Takeaways

- SDE is the #1 valuation metric for owner-operated businesses generating under $5M in revenue—used by buyers, brokers, SBA lenders, and appraisers alike

- The formula adds back owner salary, benefits, discretionary spending, depreciation, interest, and non-recurring costs to pre-tax net income

- Buyers typically apply SDE multiples of 1.5× to 4.0× depending on industry, growth trajectory, and owner dependency

- Clean, well-documented SDE builds buyer trust, secures higher multiples, and accelerates the sales process

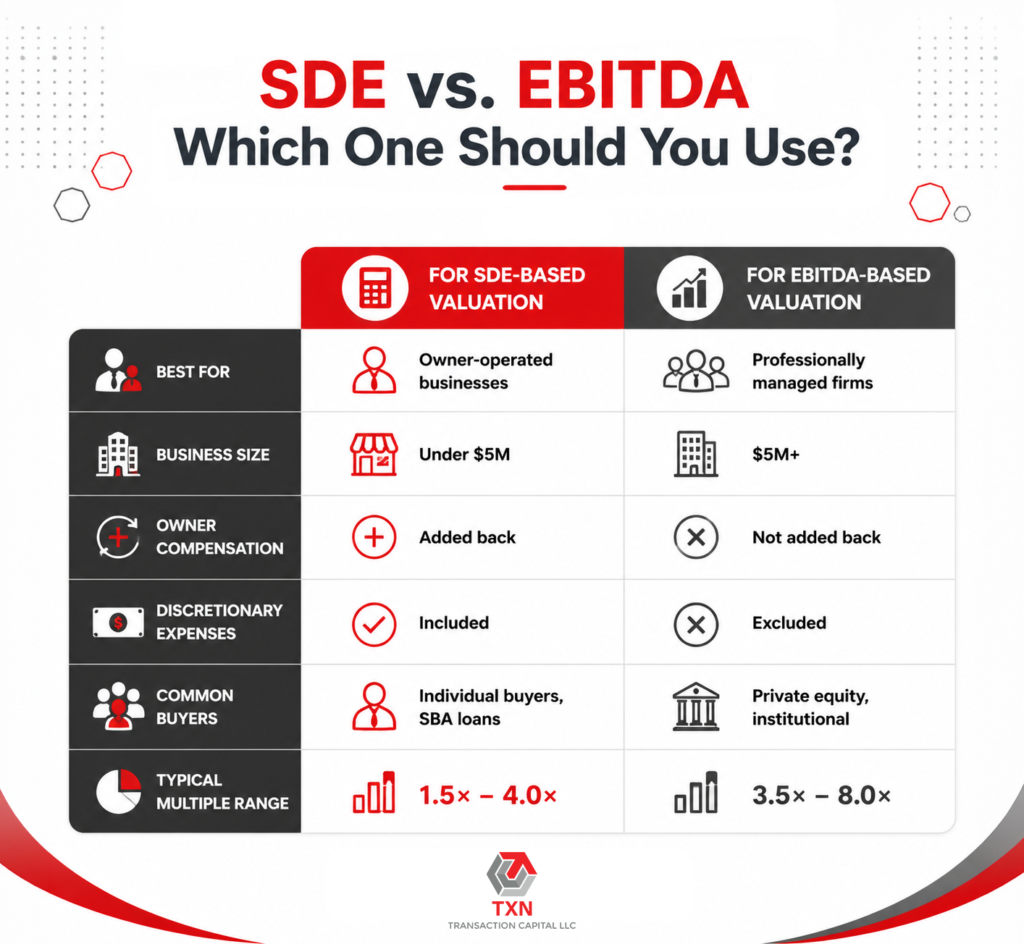

- SDE differs from EBITDA primarily in the treatment of owner compensation—use SDE when you actively manage the business, EBITDA when it operates independently of you

- Professional SDE analysis delivers audit-defensible, lender-approved documentation that self-calculated figures cannot match

What Is Seller’s Discretionary Earnings (SDE)?

Seller’s Discretionary Earnings measures the complete economic benefit that a single, full-time owner extracts from their business operations. It functions as a normalized earnings metric – a way of restating a company’s true profitability after removing the financial noise created by ownership decisions, personal spending patterns, tax strategies, and one-time events.

SDE goes well beyond simple net profit by factoring in:

- Owner’s total compensation package (salary, draws, bonuses, payroll taxes, health insurance, retirement contributions)

- Personal expenses processed through the business (vehicle use, travel, meals, cell phone)

- One-time or non-recurring costs that will not continue under new ownership

- Non-cash accounting entries such as depreciation and amortization

- Interest payments on business debt (since the new buyer’s financing structure will differ)

You may also hear SDE referred to by other names, including adjusted cash flow, owner’s benefit, recast earnings, seller’s discretionary cash flow, or total owner’s benefit. Despite the different terminology, they all describe the same concept: what does this business genuinely put in the owner’s pocket each year?

Why Is SDE Crucial for Small Businesses?

Traditional financial metrics like net income frequently understate the real economic value of owning a small business. Owners routinely run personal expenses through the company, pay themselves below-market salaries to minimize tax liability, or make one-time investments that temporarily suppress profits. Without adjustments, a buyer looking at your profit-and-loss statement sees a distorted picture that undervalues your business.

SDE corrects these distortions. It provides the standardized, apples-to-apples earnings figure that buyers, brokers, and lenders rely on to evaluate one business against another—much like how real estate agents use comparable sales to price homes.

Why Does SDE Beat Net Profit for Small Business Valuations?

Net profit alone almost always understates the authentic economic benefit of owning a small business. Business owners regularly process personal expenses through the company, set their compensation significantly above or below market rates, and absorb one-time costs that skew the numbers. Without normalizing these factors, prospective buyers see misleading results.

Consider this straightforward example:

- A landscaping business reports net profit of $60,000

- The owner also pays themselves $75,000 in salary

- The company covers a vehicle used partly for personal purposes ($8,000/year)

- A one-time legal expense hit the books last year ($5,000)

Adjusted SDE = $60,000 + $75,000 + $8,000 + $5,000 = $148,000

That $148,000 tells a fundamentally different story than $60,000 net profit. A buyer applying for a 2.5× multiple would value this business at $370,000 based on SDE versus just $150,000 based on net income. That’s a $220,000 difference – all because the earnings were properly normalized.

This is precisely why SDE is the preferred valuation metric for Main Street business sales, SBA lending decisions, and broker-mediated transactions involving owner-operated companies.

Need Expert Guidance on Your SDE Calculation?

Schedule a free 15-minute consultation with our certified appraisers to discuss your specific situation and ensure your Seller’s Discretionary Earnings are calculated accurately and defensibly.

Book Your Free 15-Minute ConsultationSDE vs. EBITDA: What’s the Difference?

Both SDE and EBITDA aim to normalize business earnings for comparison purposes, but they serve different audiences and company profiles.

Aspect | SDE | EBITDA |

Best For | Owner-operated businesses (Main Street, under $5M revenue) | Larger, professionally managed firms ($5M+ revenue) |

Owner Salary | Added back (one full-time owner-operator) | Not added back (management salaries remain as expenses) |

Discretionary Items | Included (personal travel, auto, entertainment) | Excluded |

Primary Purpose | Shows what one owner can realistically take home | Shows operational performance independent of ownership |

Typical Buyers | Individual buyers, SBA-financed purchasers, search funds | Private equity firms, strategic acquirers, institutional investors |

Typical Multiples | 1.5×–4.0× | 3.5×–8.0× (or higher for premium assets) |

The practical rule of thumb is straightforward:

- If you manage the business day-to-day and the company depends on your involvement → use SDE

- If the business operates profitably without your direct participation → use EBITDA

When Should You Transition from SDE to EBITDA?

One of the smartest moves a growing business owner can make is deliberately shifting from SDE-dependent operations to an EBITDA-friendly structure. As your company scales past $2–3 million in revenue and you install professional management, EBITDA becomes the more appropriate metric—and it opens the door to higher-caliber buyers willing to pay larger multiples.

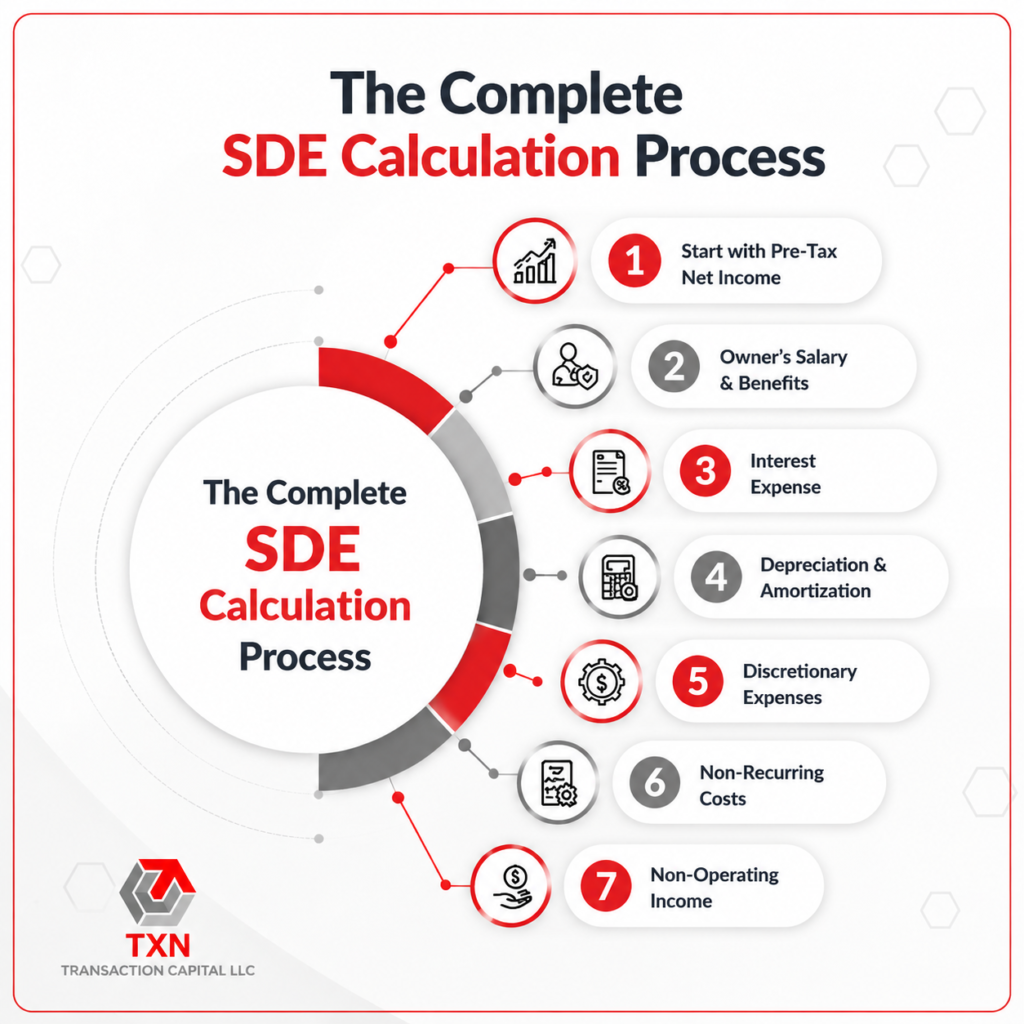

The Complete SDE Formula

Here is the full SDE calculation formula used by business brokers, certified appraisers, and SBA lenders nationwide:

SDE = Net Profit (Pre-Tax) + One Owner’s Compensation (normalized to market rate) + Interest Expense + Depreciation & Amortization + Discretionary Expenses + Non-Recurring / One-Time Expenses − Non-Operating Income ± Normalizing Adjustments (replacement salaries, related-party rent, below-market contracts)

Every component serves a specific purpose in creating a normalized earnings picture that prospective buyers can trust; lenders can underwrite, and appraisers can defend.

How to Calculate SDE: A Step-by-Step Process

Step 1: Start With Pre-Tax Net Income

Begin with your business’s net profit before taxes from your P&L statement or most recent tax return. This baseline figure represents core profitability before any owner-specific adjustments are applied.

Pro tip: Use the most recent trailing twelve months (TTM) for the most current snapshot but have 2–3 years of historical data ready. Buyers and SBA lenders want to see earnings trends, not just a single data point. If your business is growing consistently, buyers may weight recent performance more heavily. However, if growth has been uneven, some valuators apply a weighted average across multiple years.

Step 2: Add Back Owner Compensation

Include the full compensation package for one working owner-operator:

- Base salary or owner draws

- Employer-side payroll taxes

- Health and dental insurance premiums

- Retirement plan contributions (401(k), SEP-IRA, SIMPLE IRA)

- Life and disability insurance premiums paid by the business

limitation: Only add back compensation for one full-time owner-operator. If your business has multiple working owners, you must subtract fair-market replacement salaries for every additional owner beyond the first. Ignoring this adjustment is one of the most common—and damaging mistakes in SDE calculations.

Step 3: Add Back Financing and Non-Cash Costs

These items get added back because they reflect ownership-specific financial decisions rather than operational performance:

- Interest expense on business loans, lines of credit, and equipment financing

- Depreciation on physical assets (equipment, vehicles, buildings)

- Amortization of intangible assets (patents, customer lists, purchased goodwill)

New owners will structure financing differently and carry their own depreciation schedules, so these figures don’t reflect the business’s true cash-generating ability.

Step 4: Add Back Discretionary Business Expenses

Include personal expenses legitimately processed through the company:

- Personal use of company vehicles (or the personal-use portion of mixed-use vehicles)

- Owner’s personal cell phone bills

- Personal meals, entertainment, and travel

- Charitable donations made through the business

- Country club or gym memberships

- Owner-only perks (season tickets, subscriptions, personal education not tied to operations)

Documentation requirement: Every discretionary add-back should be supported with receipts, invoices, or expense reports with clear business justification. Buyers scrutinize add-backs heavily undocumented claims erode trust and reduce your negotiating leverage.

Step 5: Account for Non-Recurring Expenses

One-time costs that will not repeat under new ownership:

- Legal settlement payments or lawsuit defense costs

- Emergency equipment repairs or disaster recovery expenses

- One-time consultant or advisory fees for specific projects

- Unusual insurance claims or premium spikes

- Moving or relocation costs

- Website redesign or major technology overhaul expenses

Buyer scrutiny warning: Expect pushback on anything classified as “non-recurring.” Sophisticated buyers and their advisors will challenge whether expenses are genuinely one-time, or simply cyclical costs rebranded to inflate SDE.

Step 6: Subtract Non-Operating Income

Remove income that will not transfer to a new owner:

- Insurance settlement proceeds

- Gains from selling business assets unrelated to operations

- Investment income earned on excess business cash

- Rental income from properties unrelated to the core business

- Government grants or pandemic-era relief payments that have expired

Step 7: Apply Normalizing Adjustments

Adjust for arrangements that deviate from fair market terms:

- Related-party rent: If the owner also owns the building and charges the business above or below market rent, normalize to market rates

- Family member salaries: If family employees are paid above or below market wages, adjust to competitive compensation levels

- Unusual supplier arrangements: Favorable or unfavorable terms that would not continue post-sale

- Below-market customer contracts: Long-term contracts priced below current market rates that will reset upon ownership change

Audit-Ready Valuation Reports in Just 2–5 Business Days

Transaction Capital’s ABV® and ASA certified professionals deliver defensible valuation reports starting at $500. Get the clarity you need for investors, transactions, or compliance.

Get Your Valuation QuoteReal-World SDE Calculation Examples

Example 1: Small Restaurant

Component | Amount |

Net Profit (Pre-Tax) | $120,000 |

+ Owner Salary | $80,000 |

+ Interest Expense | $10,000 |

+ Depreciation | $7,000 |

+ Discretionary Expenses (auto + personal travel) | $12,000 |

+ One-Time Legal Fees | $8,000 |

= SDE | $237,000 |

At an industry-typical multiple of 2.5×, this restaurant would be valued at approximately $592,500.

Example 2: HVAC Service Business

Component | Amount |

Pre-Tax Income | $275,000 |

+ Owner Salary | $85,000 |

+ Interest Expense | $12,000 |

+ Depreciation & Amortization | $18,000 |

+ Owner Perks | $22,000 |

+ One-Time Renovation | $8,000 |

= SDE | $420,000 |

Applying a 3.0× multiple for an established HVAC company with recurring service contracts → business value of approximately $1,260,000.

Example 3: Joe’s Auto Repair

Component | Amount |

Net Income | $75,000 |

+ Depreciation & Amortization | $10,000 |

+ Interest | $5,000 |

+ One-Time Expense | $2,500 |

+ Owner’s Salary & Perks | $68,000 |

− Non-Discretionary Owner Rent | −$12,000 |

= SDE | $138,500 |

An industry-appropriate multiple of 2.8× → estimated valuation of approximately $387,800.

What Expenses Can You Legitimately Add Back?

Not all add-backs are created equally. Buyers, brokers, and SBA loan officers categorize adjustments by their defensibility.

1. Clearly Acceptable Add-Backs

These adjustments are universally recognized and rarely challenged:

- One owner’s complete compensation package (salary, taxes, benefits, retirement)

- All depreciation and amortization

- Interest expense on business debt

- Documented one-time legal or professional fees with clear supporting evidence

- Personal use of company vehicles (with mileage logs or documented split)

- Owner-specific insurance policies (life, disability, supplemental health)

2. Questionable Add-Backs Requiring Strong Justification

These require thorough documentation and clear, logical rationale:

- Mixed-use travel expenses (you must separate personal vs. business portions convincingly)

- Entertainment expenses exceeding normal business hosting needs

- Charitable contributions made through the business

- Home office expenses for the owner’s personal residence

- Professional development courses with primarily personal benefit

- Family member cell phone plans paid by the business

3. Completely Unacceptable Add-Backs

Including these will damage your credibility with any serious buyer:

- Regular employee salaries for non-owner staff

- Ongoing marketing and advertising expenditures

- Normal, recurring maintenance and repair costs

- Multiple owner salaries beyond one full-time equivalent

- Expenses that directly support ongoing business operations

- Recurring utility bills and standard operational overhead

Common SDE Calculation Mistakes to Avoid

1. Overstating “One-Time” Costs

Classifying recurring expenses as non-recurring is the fastest way to lose a buyer’s trust. If your “one-time” legal fees show up three years running, sophisticated buyers will immediately reclassify them as operating expenses and reduce your SDE accordingly.

2. Ignoring Owner Replacement Salaries

When multiple owners actively work in the business, failing to deduct market-rate replacement salaries for additional owners beyond the first inflates SDE artificially. Buyers recognize this instantly, and it undermines the credibility of your entire financial presentation.

3. Insufficient Documentation

Every add-back must be supported by receipts, invoices, bank statements, or payroll records. Buyers and SBA lenders may reject undocumented adjustments entirely—potentially reducing your calculated SDE by tens of thousands of dollars.

4. Overlooking CapEx and Working Capital Requirements

SDE adds back depreciation, which creates the impression of higher cash flow. But for asset-heavy businesses (manufacturing, construction, restaurants), equipment eventually needs replacement. Buyers model capital expenditures and working capital separately and failing to account for these requirements can make your business appear stronger than it truly is, leading to valuation disputes during due diligence.

5. Mixing Personal and Business Finances

Blending personal transactions with business accounts makes normalization exponentially harder. It reduces transparency, increases audit risk, and signals to buyers that the financial records may be unreliable—directly lowering the multiples they’re willing to pay.

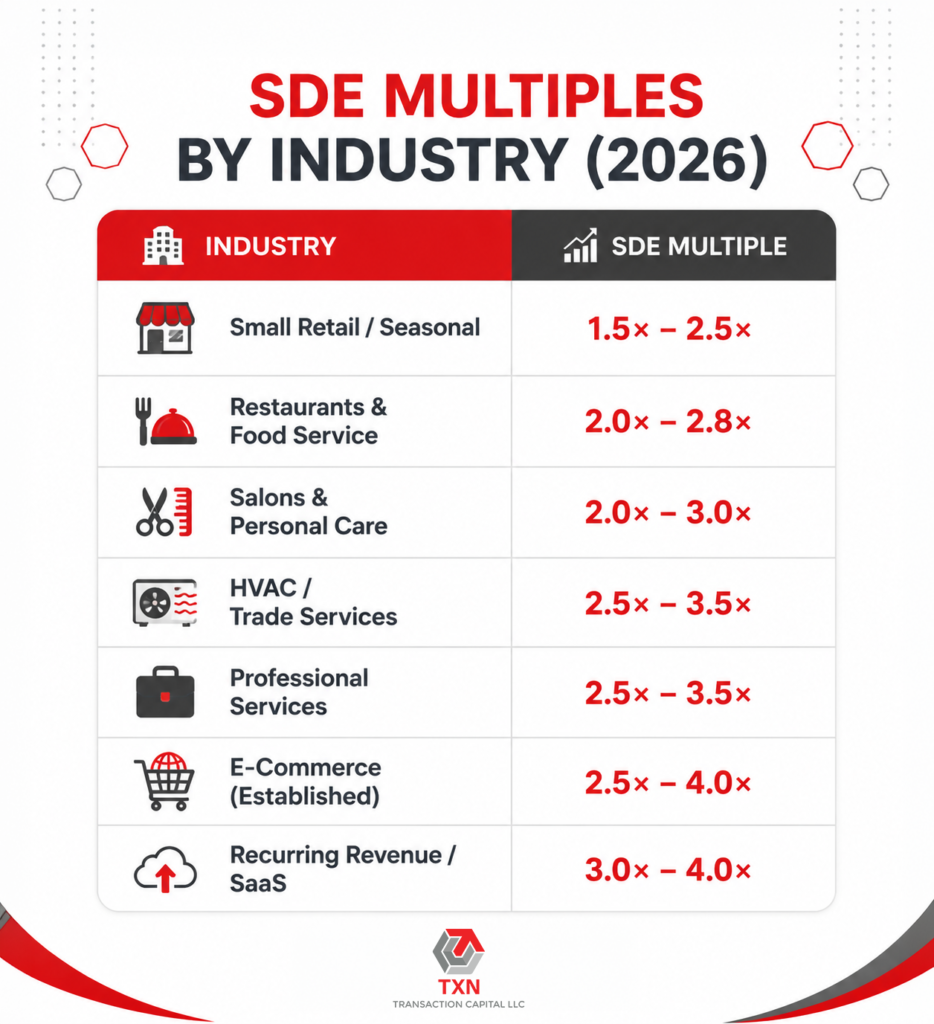

What Are Typical SDE Multiples in Industry?

Once you have calculated an accurate SDE figure, valuation becomes a multiplication exercise. Business brokers, certified appraisers, and buyers apply industry-specific multiples to determine fair market value.

Here are typical SDE multiple ranges:

Lower Multiples (1.5×–2.5×)

- Small retail shops and convenience stores

- Seasonal businesses (landscaping, holiday retail)

- Location-dependent services with limited transferability

- Businesses with high owner dependency and minimal documented systems

Medium Multiples (2.0×–3.0×)

- Restaurants and food service operations

- Salons, spas, and personal care services

- Traditional trade services (plumbing, electrical, painting)

- General service businesses with moderate recurring revenue

Higher Multiples (2.5×–4.0×)

- Recurring revenue businesses (SaaS under $1M, subscription services)

- Professional services firms (accounting, consulting, staffing)

- E-commerce operations with established supply chains and brands

- Technology-enabled service companies

- Businesses with documented SOPs and minimal owner involvement

Key factors that push multiples higher: recurring revenue, diversified customer base, documented processes, strong growth trajectory, low owner dependency, clean financial records, and favorable industry trends.

Key factors that compress multiples: heavy owner reliance, customer concentration, inconsistent earnings, poor documentation, declining industry, and deferred maintenance or capital needs.

How Does SDE Factor SBA Lending?

For buyers financing acquisitions through SBA 7(a) loans—the most common lending vehicle for Main Street business purchases—SDE is a critical underwriting metric. SBA lenders require that the business generate sufficient cash flow to service acquisition debt while also providing the new owner with reasonable compensation.

Lenders typically want to see a debt service coverage ratio (DSCR) of 1.15× to 1.25× or higher, calculated using the business’s SDE minus a normalized owner’s salary. This means the remaining earnings after a fair owner’s salary must cover annual debt payments with a comfortable margin.

A professionally prepared SDE analysis from a certified valuation firm gives SBA lenders the confidence to approve financing at favorable terms, while self-calculated figures often trigger additional documentation requests or outright skepticism.

Understanding the Limitations of SDE

While SDE is the standard valuation metric for small businesses, it has acknowledged limitations that sophisticated buyers account for:

1. Depreciation of distortion for asset-heavy businesses. Adding back depreciation inflates apparent earnings for companies that require ongoing equipment replacement. A trucking company adding back $80,000 in depreciation may need to spend $90,000 on fleet replacement next year—making the SDE figure misleading without separate CapEx analysis.

2. SDE is not true for post-acquisition cash flow. Because it adds back interest and ignores the buyer’s likely debt service, SDE overstates what a leveraged buyer will pocket. Buyers adjust their expected financing costs when converting SDE into an offer price.

3. Subjectivity in add-back classification. Reasonable people can disagree about whether specific expenses are truly discretionary or one-time. This subjectivity is why professional, third-party SDE analysis from credentialed appraisers carries far more weight than owner-prepared calculations.

How to Maximize Your SDE Before Selling

Strategy 1: Clean Up Financial Records Early

Start separating personal and business expenses 18–24 months before putting your company on the market. Open dedicated personal credit cards, stop running personal costs through business accounts, and document any remaining mixed-use expenses with detailed records.

Strategy 2: Normalize Owner Compensation

Ensure your salary reflects fair market rates for comparable roles in your industry and region. Compensation that is dramatically above or below market raises immediate red flags for buyers and their advisors.

Strategy 3: Build Operational Independence

Reduce business dependency on your daily involvement by documenting all processes, training key employees, and building management systems that function without you. Businesses with lower owner dependency consistently earn higher SDE multiples and attract a broader buyer pool, including institutional investors.

Strategy 4: Prioritize Recurring Revenue

Revenue sources with predictable, repeating patterns dramatically increase both SDE multiples and buyer confidence:

- Service contracts with annual renewal terms

- Subscription-based service offerings

- Maintenance agreements with existing clients

- Retainer relationships with long-term customers

Strategy 5: Improve Profit Margins Systematically

Focus on operational efficiency improvements well before your exit:

- Renegotiate supplier terms and bulk pricing arrangements

- Eliminate unnecessary overhead and redundant expenses

- Implement productivity-enhancing technology

- Review and optimize your pricing strategy based on current market conditions

- Streamline workflows to reduce waste and inefficiency

Strategy 6: Start the Process 24–36 Months Early

Begin SDE optimization in advance of your planned sale. Establish clean record-keeping systems, separate all personal expenses, build consistent performance metrics, and create comprehensive operational documentation. The earlier you start, the more credible your financial story becomes.

Advanced SDE Considerations for Complex Businesses

1. Multiple Revenue Streams

For businesses with diverse income sources, such as a restaurant that also offers catering, merchandise, and event space rental calculate SDE for core operations separately from ancillary and passive income. This segmentation provides cleaner comparables and helps buyers understand which revenue streams are truly transferable.

2. Seasonal Business Adjustments

Highly seasonal businesses demand careful normalization. Use rolling 12-month periods instead of calendar years, adjust for unusual weather or external market disruptions, and present multiple years of data so buyers can identify genuine trends versus seasonal noise.

3. Family Business Complexities

Family-owned companies frequently present unique SDE challenges: multiple family members on payroll at non-market rates, related-party transactions for real estate or supplies, and blurred boundaries between personal and business assets. Working with experienced valuation professionals who understand family business dynamics ensures that normalizations are both accurate and defensible.

4. Weighted Average SDE Across Multiple Years

Depending on earnings consistency, buyers and appraisers may calculate a weighted average SDE across 2–3 years rather than relying solely on TTM figures. Common weighting approaches assign the most recent year to the heaviest weight (e.g., 50% for Year 1, 30% for Year 2, 20% for Year 3). This smooths out anomalies and provides a more reliable earnings baseline for valuation.

When Should You Hire Professional Valuation Services?

While basic SDE calculations can inform your planning, certified valuations provide the defensibility and credibility required for formal transactions.

Situations That Require Professional Valuations

- SBA loan applications: Lenders demand certified business valuations meeting specific USPAP or NACVA standards

- Business sale preparation: Professional valuations identify hidden value drivers, optimization opportunities, and realistic pricing expectations

- Partnership disputes and buyouts: Court-admissible valuations require credentialed appraisers (CVA®, ASA, ABV®) who can provide expert testimony

- Estate planning and gift tax compliance: IRS-compliant valuations must meet Revenue Ruling 59-60 requirements

- Divorce proceedings: Forensic valuation distinguishes enterprise goodwill from personal goodwill and normalizes earnings for equitable distribution

- Tax compliance and audit defense: Professional valuations backed by certified appraisers provide a defensible position in IRS examinations

Why Choose Certified Valuation Professionals?

At Transaction Capital LLC, our team holds multiple industry certifications that ensure every report meets the highest professional standards:

- ABV® (Accredited in Business Valuation) from the AICPA

- ASA (Accredited Senior Appraiser) from the American Society of Appraisers

- CVA® (Certified Valuation Analyst) from NACVA

- MRICS from the Royal Institution of Chartered Surveyors

Our expertise spans business valuation services, startup valuations, ESOP valuation services, gift & estate tax valuations, divorce valuations, and litigation valuation support.

Conclusion

Understanding how to calculate seller’s discretionary earnings gives you powerful, actionable insight into your business’s true worth. Whether you are planning to sell, pursuing SBA financing, navigating a partnership transition, or simply tracking value creation year over year, accurate SDE analysis forms the foundation for confident, informed decision-making.

Success in maximizing your business value lies in preparation and documentation. Start cleaning up financials, separating personal expenses, building operational independence, and documenting processes well before you need a formal valuation. The owners who achieve the strongest exit outcomes are those who treat SDE optimization as an ongoing discipline, not a last-minute exercise.

Ready to discover your business’s true value? Transaction Capital LLC specializes in certified, audit-defensible business valuations.

Start with a Free 15-Minute Valuation Consultation

Discuss your valuation needs with our certified experts. Reports are delivered in 2–5 business days, and you can review the draft before paying to ensure complete transparency.

Book Your Free ConsultationFrequently Asked Questions About Seller’s Discretionary Earnings

1. What’s the difference between SDE and the owner’s cash flow?

SDE is a pre-tax, normalized earnings metric, while owner’s cash flow accounts for taxes, capital expenditures, and working capital changes. SDE measures earning potential; cash flow reflects actual money available after all obligations.

2. How do buyers use SDE to determine purchase prices?

Buyers apply industry-specific multiples (commonly 1.5×–4.0×) to SDE to estimate initial business value, then adjust for financing requirements, growth potential, risk profile, and deal structure. SDE serves as the starting foundation for all subsequent negotiations.

3. How many years of SDE data should I prepare?

Most buyers and SBA lenders want the trailing twelve months (TTM) plus 2–3 years of historical figures. This reveals earnings trends, seasonal patterns, and any unusual years requiring explanation or normalization.

4. Can I add back all personal expenses to run through the business?

Only legitimate business expenses with documented personal benefit qualify as add-backs. Purely personal costs like family groceries, personal vacations, or non-business entertainment should never appear in SDE calculations. Every adjustment requires clear documentation and business justification.

5. When should I use SDE instead of EBITDA for my business?

Use SDE if you actively manage the business day-to-day, and the company depends on your involvement. Transition to EBITDA once the business operates profitably under professional management without your direct participation—typically above $2–3M in revenue.

6. Is a professionally prepared SDE analysis worth the cost?

For any significant transaction – selling, SBA lending, litigation, estate planning—professional analysis provides credibility, defensibility, and accuracy that self-calculated figures cannot match. Certified valuations are accepted by lenders, courts, and the IRS; DIY calculations typically are not.

7. How does SDE affect SBA loan approval?

SBA lenders use SDE to calculate debt service coverage ratios (DSCR). They subtract a normalized owner salary from SDE and verify the remaining earnings can cover annual loan payments with a margin of 1.15×–1.25× or more. Professionally documented SDE analysis strengthens loan applications significantly.

8. What SDE multiple should I expect for my industry?

Multiples vary significantly. Retail and seasonal businesses typically trade at 1.5×–2.5× SDE, service businesses at 2.0×–3.0×, and recurring revenue or technology-enabled businesses at 2.5×–4.0×. Specific multiples depend on profitability, growth, customer concentration, owner dependency, and market conditions.