409A Valuation Report – Sample, Structure & What to Expect (Transaction Capital LLC)

Let’s begin by understanding what a 409A valuation report is, and explore a Transaction Capital LLC sample report to see how it works.

Companies, especially startups use 409A valuations to determine the fair market value (FMV) of their common stock for issuing employee stock options. This means the 409A valuation report establishes the strike price of stock options in compliance with IRC Section 409A.

This report must be prepared by an independent qualified valuation firm to ensure accuracy and to obtain IRS Safe Harbor protection. To achieve a defensible valuation, it is essential to engage a firm that follows International Valuation Standards (IVS), USPAP, and AICPA SSVS-1.

At Transaction Capital LLC, all reports are prepared and signed by ABV®, ASA®, CVA®, and MRICS® credentialed professionals, ensuring audit-ready, IRS-compliant valuations.

What is a 409A Valuation Report?

A 409A valuation report determines the fair market value (FMV) of a private company’s common stock for tax compliance and stock-based compensation purposes.

This valuation is performed on a:

- IRC Section 409A

- IRS Revenue Ruling 59-60 (FMV definition)

- Going concern premise of value

- Minority, non-marketable basis

Get Your Free 409A Valuation Report Sample

See how a professionally structured 409A valuation report looks in real-world scenarios. This sample from Transaction Capital LLC highlights format, methodology, and compliance-ready documentation.

Download Sample Report →Importance and Use of Valuation Report

A 409A valuation report is essential for IRS compliance and Safe Harbor protection, ensuring that a company meets IRC 409A requirements and avoids severe tax consequences such as immediate taxation, 20% penalties, and interest charges. It provides a defensible fair market value (FMV) of common stock, helping companies stay compliant and audit-ready.

It also plays a critical role in stock option pricing and strategic decision-making, as it determines the exercise price for employee equity while offering insights into enterprise value, capital structure, and investor benchmarks.

Additionally, when prepared by qualified professionals (ABV®, ASA®, CVA®), the report supports audit defense and financial reporting (ASC 718), ensuring credibility with auditors, investors, and regulators.

When is a 409A Valuation Required?

A company must obtain a 409A valuation:

- At least once every 12 months

- Before issuing first stock options

- After material events, including:

- Funding rounds (SAFE, preferred equity, convertible notes)

- M&A or strategic transactions

- Significant financial changes

- IPO preparation

409A Valuation Report Sample & Example (IRS-Compliant – Transaction Capital LLC)

There is no prescribed IRS template for a 409A valuation report. However, to obtain Safe Harbor protection, the valuation must comply with IRC Section 409A, Treasury Regulations §1.409A-1(b)(5)(iv), and Revenue Ruling 59-60, along with recognized professional standards including USPAP, AICPA SSVS-1, NACVA, and IVS. The valuation must be performed by an IRS-qualified independent appraiser, meaning an individual with relevant education, training, and experience in similar valuations, and who is independent of the company. A defensible report requires appropriate methodology selection, consistent assumptions, and thorough documentation.

At Transaction Capital LLC, 409A valuation reports are prepared in a 40–80 page audit-ready format, incorporating income (DCF), market, and option-based approaches (OPM, PWERM), as applicable. The analysis includes equity value allocation across multiple share classes, reflecting capital structure complexities such as SAFEs, convertible notes, and preferred equity. Appropriate Discount for Lack of Marketability (DLOM) is applied to reflect illiquidity of private company shares, while Discount for Lack of Control (DLOC) is considered where relevant to minority interests. Multiple methodologies are evaluated and reconciled to ensure a robust and supportable conclusion. Each report is signed by ABV®, ASA® & CVA®, credentialed valuers, ensuring IRS-compliant, audit-defensible, and institutionally reliable valuations.

Transaction Capital LLC – 409A Valuation Report Structure

1. Transmittal Letter

This section formally defines the engagement, valuation date, and purpose (IRC 409A compliance). It clearly states that the valuation is prepared independently and is intended only for specific use.

It also includes Safe Harbor positioning, independence declaration, and confirmation that the report is prepared by a qualified valuation firm following USPAP and SSVS-1 standards, which many low-cost providers fail to explicitly disclose.

2. Background

The background section defines the Fair Market Value (FMV) as per IRS Revenue Ruling 59-60 and clarifies that the valuation is done on a minority, non-marketable, going concern basis, which is standard for 409A purposes.

It also outlines the scope, procedures, and key data sources used, including financials, projections, and cap table. Proper documentation is critical here many valuers miss clear support for assumptions and inputs, which can weaken the report during audit or IRS review.

3. Overview of Valuation

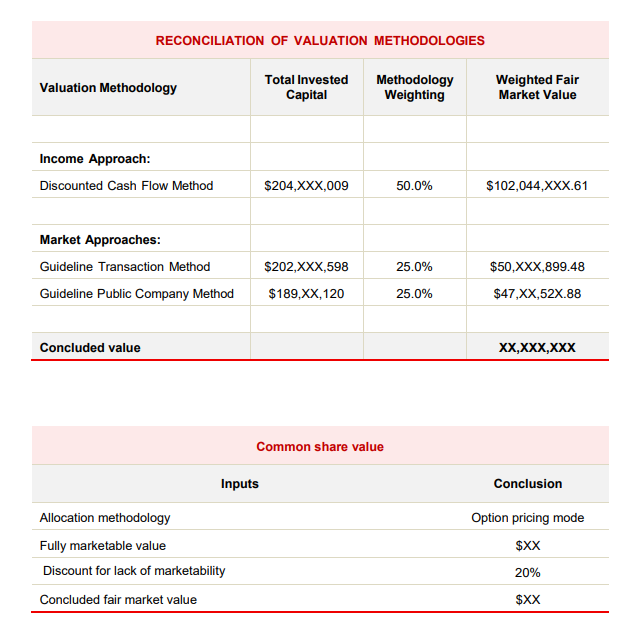

This section summarizes valuation approaches used and presents the reconciliation of methods leading to the final enterprise value.

A strong report clearly explains weighting logic. Weak reports often apply arbitrary weights without justification, which can fail under audit scrutiny.

A strong report clearly explains weighting logic. Weak reports often apply arbitrary weights without justification, which can fail under audit scrutiny.

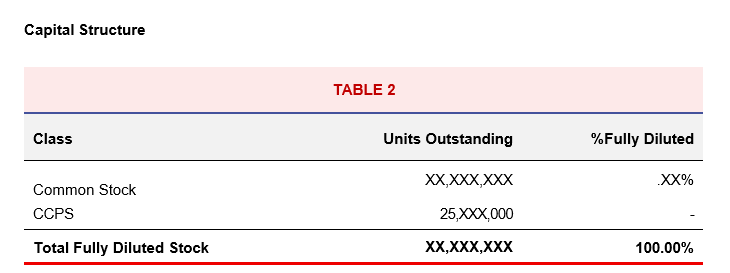

4. Corporate Profile & Capital Structure

This section provides a detailed overview of the company’s business model, products, revenue streams, target customers, and competitive positioning, along with insights into management strength, SWOT analysis, and stage of development. It helps establish the company’s operational context and growth trajectory, which directly influence valuation assumptions.

It also includes a detailed fully diluted cap table, covering all equity classes, including common, preferred, SAFEs, and convertible instruments. Proper treatment of liquidation preferences, conversion terms, and capital stack hierarchy is critical, as these determine how value is allocated across securities. Any simplification or misclassification can materially distort equity allocation and result in an incorrect FMV that may not withstand audit or investor review.

5. Financial Statement Analysis

This section includes detailed historical and projected financials, highlighting revenue growth, margins, cost structure, and cash flow trends, which form the foundation for valuation methods such as DCF.

Accurate and consistent financials are critical, as valuation is highly sensitive to projections and assumptions. Proper normalization, reconciliation, and alignment of data ensure reliability. Common mistakes include using incomplete projections, inconsistent formats, or unsupported assumptions, which can significantly distort valuation outcomes and weaken audit defensibility.

6. National Economy

This section evaluates macroeconomic conditions such as GDP, inflation, and interest rates, which directly impact discount rates and valuation assumptions.

Ignoring macroeconomic context is a common mistake that leads to unrealistic valuation conclusions.

7. Industry Analysis

Provides insights into industry growth, competition, and market trends, helping benchmark the company against peers.

Strong valuation reports use data-backed industry analysis, while weaker reports rely on generic descriptions without relevance to valuation inputs.

8. Overview of Business Valuation

This section explains the three primary approaches income, market, and cost and their applicability based on the company’s stage, financial profile, and availability of data.

A critical aspect is method selection and justification. Many valuers rely on standard templates without assessing relevance, apply inappropriate methods (e.g., using market multiples for early-stage companies with no revenue), or fail to reconcile results across approaches. Such mistakes can lead to unsupported conclusions and reduce the defensibility of the valuation.

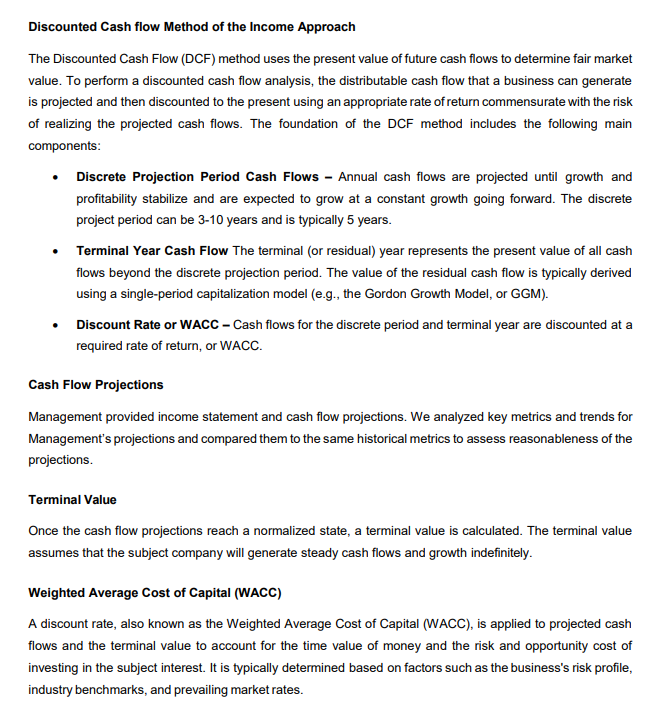

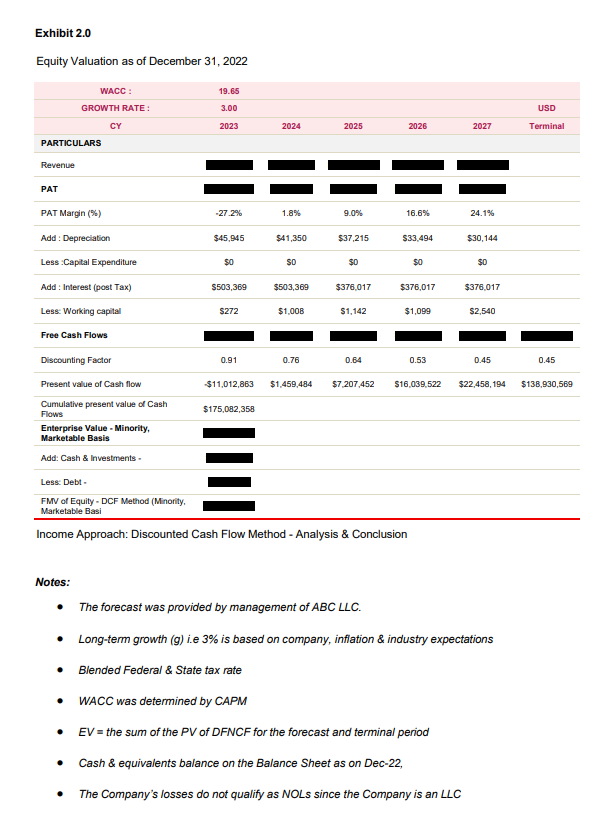

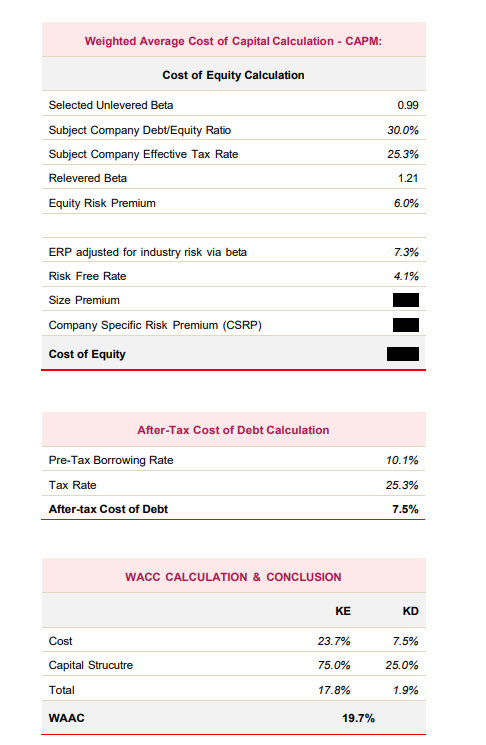

9. Income Approach

The DCF method evaluates future cash flows and discounts them to present value using a risk-adjusted discount rate, making it one of the most critical drivers of valuation.

This is one of the most scrutinized areas in audits. Common mistakes include overly optimistic projections, inconsistent cash flow assumptions, incorrect discount rate selection, and unrealistic terminal growth rates. Even small errors in these inputs can materially distort valuation and weaken audit defensibility.

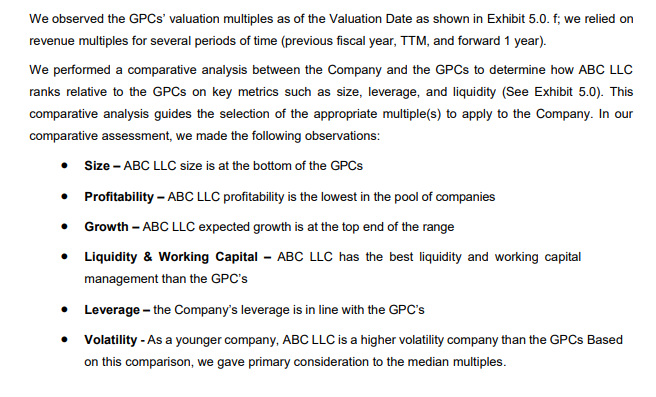

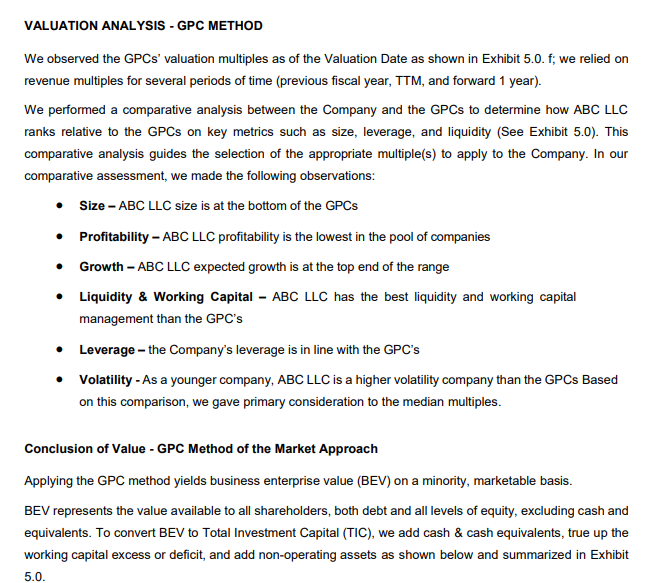

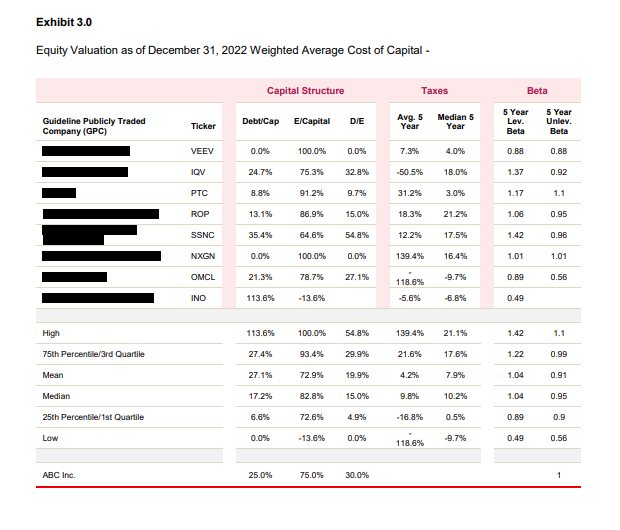

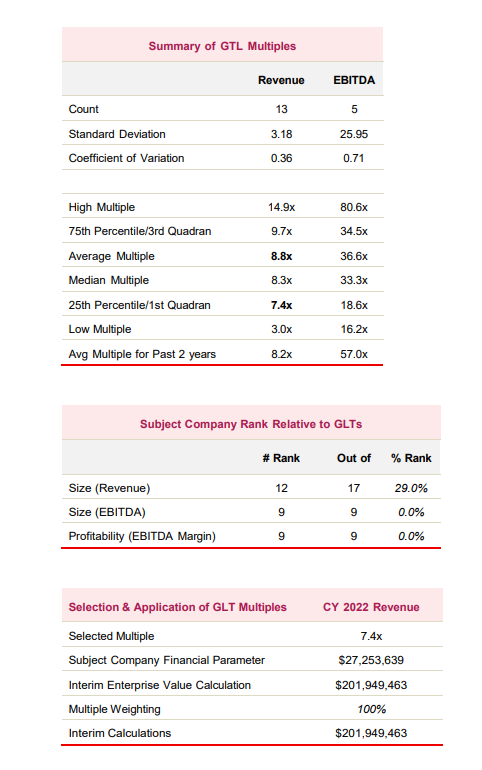

10. Market Approach

The market approach derives valuation multiples using both guideline public companies (GPC) and comparable transactions (Guideline Transaction Method). Public company multiples are adjusted for differences in size, growth, and profitability, while transaction data provides real-world benchmarks based on actual deal activity.

Proper peer selection and normalization are critical. Common mistakes include using irrelevant comparables, relying on outdated or inconsistent data, failing to adjust for margin and scale differences, and blindly applying average multiples. These issues can result in inflated or unsupported valuations that may not withstand audit or investor scrutiny.

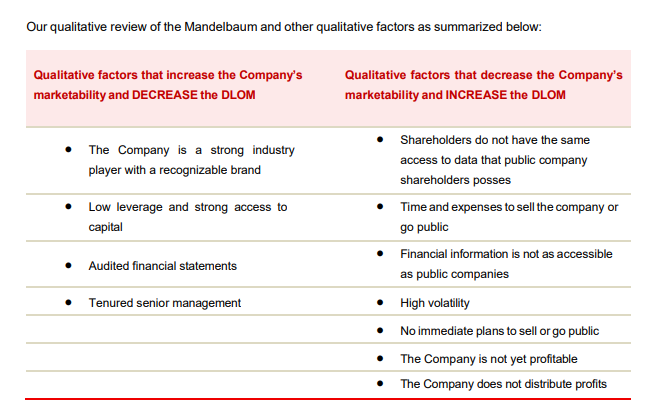

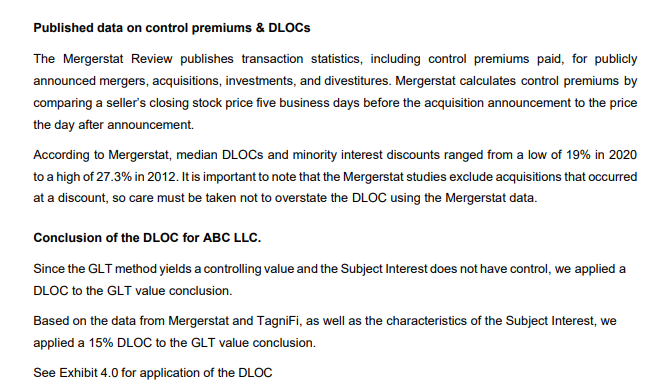

11. Discount for Lack of Marketability (DLOM)

DLOM adjusts for the illiquidity of private company shares, as such securities cannot be easily sold in the open market.

This is a critical IRS focus area. Proper DLOM must be supported by empirical studies or option pricing models. Common mistakes include applying arbitrary flat discounts (e.g., 20–30%) without support, ignoring company-specific factors like exit timeline or volatility, and double-counting risk already captured in the discount rate. Such errors can make the valuation difficult to defend during audit.

12. Discount for Lack of Control (DLOC)

DLOC reflects the reduced value of a minority ownership interest, as such investors lack control over key decisions like dividends, strategic direction, and exit timing.

Proper application of DLOC is important to align with a minority, non-controlling valuation premise. Common mistakes include ignoring DLOC entirely, applying arbitrary percentages without support, or double-counting control discounts already embedded in valuation methods. Such errors can misstate FMV and weaken the defensibility of the valuation.

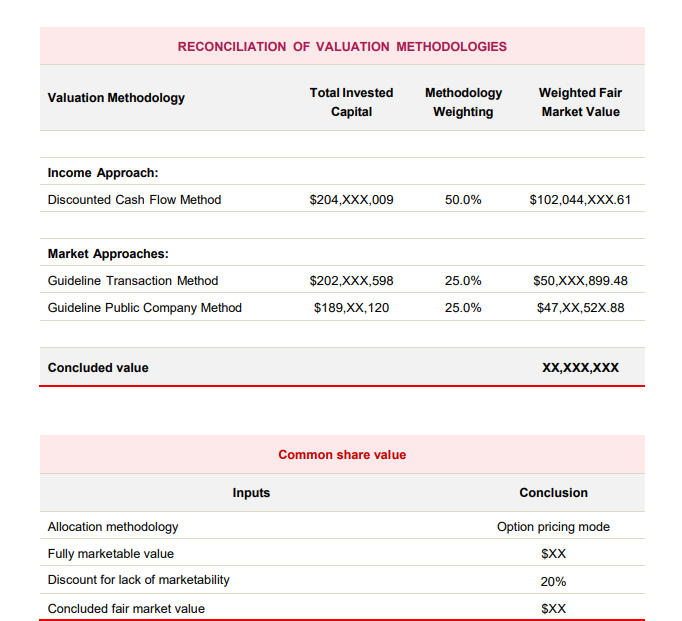

13. Synthesis of Valuation Methods

This section reconciles results from all applied valuation approaches and determines the final enterprise value based on their relative reliability and relevance.

A strong report clearly explains the weighting rationale and consistency across methods. Common mistakes include arbitrary weighting, selectively favoring one method to justify a desired outcome, or failing to reconcile differences between approaches. Such issues can undermine the credibility and audit defensibility of the valuation.

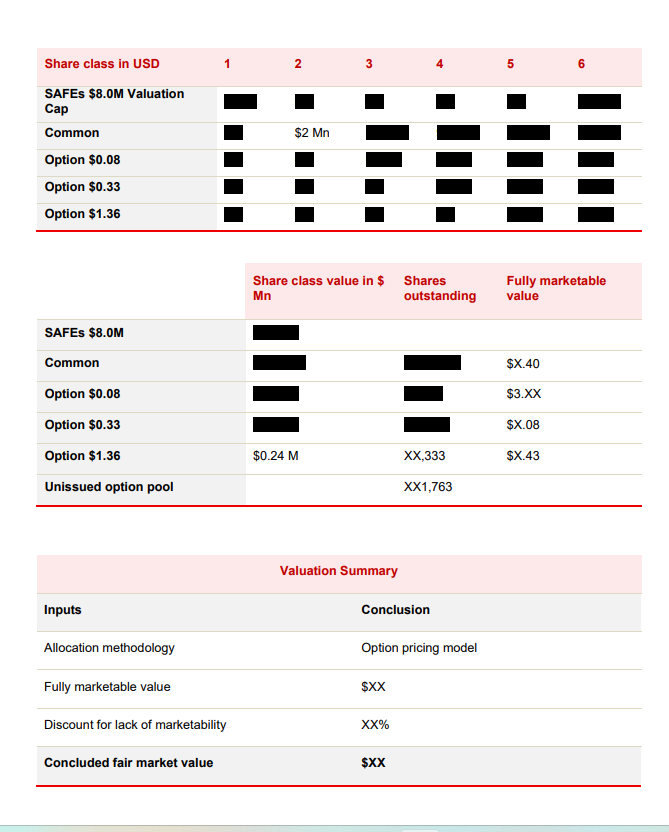

14. Allocation of Equity

This section allocates enterprise value across equity classes using models like Option Pricing Model (OPM) or PWERM.

This is one of the most important sections in a 409A valuation. Incorrect allocation especially ignoring liquidation preferences or convertibles is a major mistake made by inexperienced valuers.

15. Valuation Conclusion

This section presents the final enterprise value and fair market value (FMV) per common share, derived after applying all valuation methodologies, adjustments, and discounts.

The conclusion must be fully consistent with the underlying assumptions, methodologies, and capital structure. Common mistakes include mismatches between calculations and final outputs, incorrect share counts, or ignoring allocation adjustments any of which can raise red flags during audit or investor review.

16. Assumptions & Limiting Conditions

This section outlines all key assumptions used in the valuation and defines the scope, reliance on management data, and limitations on the use of the report.

Clear and transparent disclosure is essential for USPAP and AICPA SSVS-1 compliance, protecting both the valuer and the company. Common mistakes include incomplete disclosures, vague assumptions, or missing scope limitations, which can weaken audit defensibility and expose the valuation to challenge.

17. Appraisal Certification

This section confirms that the valuation has been prepared independently, objectively, and in accordance with professional standards such as USPAP and AICPA SSVS-1.

It is critical for audit defensibility and IRS Safe Harbor qualification, as it establishes the credibility of the report and the independence of the valuer. Common mistakes include missing certification language, lack of standard references, or unclear independence disclosures, which can weaken the report’s reliability during audit or regulatory review.

18. Valuer Qualifications

This section highlights the credentials, experience, and professional standing of the valuation expert, which is a key factor in establishing IRS Safe Harbor defensibility.

Transaction Capital LLC reports are signed by Dr. Gaurav B. (ABV®, ASA®, CVA®, MRICS®), reflecting deep expertise in IRS-compliant valuations and adherence to USPAP, AICPA SSVS-1, NACVA, and IVS standards. Proper disclosure of valuer qualifications and adherence to recognized professional standards enhances the credibility of the report and supports its defensibility in the event of audit scrutiny.

19. Appendices

The appendices include detailed supporting information used in the valuation, such as guideline company data (including trading multiples and financial benchmarks), company financial statements, and valuation working schedules.

It also contains a summary of the equity allocation methodology (e.g., Option Pricing Model or PWERM) and supporting calculations. This section is important for transparency and audit support many valuers provide limited backup, making it difficult to validate the valuation during review.

Why Transaction Capital LLC Stands Out

Transaction Capital LLC delivers IRS Safe Harbor 409A valuations with a strong focus on technical rigor, regulatory compliance, and audit readiness. Each engagement is led by certified valuation professionals (ABV®, ASA®, CVA®, MRICS®) and prepared in accordance with USPAP, AICPA SSVS-1, NACVA, and IVS standards.

Our approach emphasizes accurate capital structure analysis, proper application of DLOM and DLOC, and robust equity allocation using OPM/PWERM methodologies. Unlike template-driven providers, every valuation is custom-built, fully documented, and designed to withstand IRS, auditor, and investor scrutiny.

Conclusion

A 409A valuation is not merely a compliance requirement, it is a highly technical, audit-sensitive financial exercise that directly impacts equity pricing, tax exposure, and financial reporting.

Engaging a qualified firm like Transaction Capital LLC ensures that the valuation is accurate, defensible, and fully aligned with IRS Safe Harbor standards, protecting both the company and its stakeholders from regulatory and financial risk.

FAQs – 409A Valuation

1. What is the purpose of a 409A valuation report?

The purpose of a 409A valuation is to determine the fair market value (FMV) of a private company’s common stock for setting stock option strike prices, ensuring compliance with IRC Section 409A, and obtaining Safe Harbor protection against IRS penalties.

2. What are the key components of a 409A valuation report?

A comprehensive report includes valuation summary, financial analysis, valuation methodologies (DCF, market approach), equity allocation, assumptions, certification, and supporting exhibits, along with detailed documentation for audit support.

3. What are the risks of not having a 409A valuation?

Failure to obtain a proper 409A valuation can result in significant IRS penalties, including immediate taxation of deferred compensation, additional 20% penalties, interest charges, and reputational and legal risks.

4. How to choose the right 409A valuation provider?

Companies should select a provider with certified valuers (ABV®, ASA®, CVA®), USPAP and SSVS-1 compliance, strong audit track record, and experience with complex capital structures. A credible provider should also offer defensible reports and post-valuation support during audits.

5. How much does a 409A valuation cost?

The cost of a 409A valuation typically depends on the company’s stage and capital structure complexity. Early-stage companies with simple structures generally incur lower fees, while companies with SAFEs, preferred stock, or multiple rounds require more detailed analysis.

6. Do you provide a sample 409A valuation report?

Yes, Transaction Capital LLC provides sample reports upon request to demonstrate structure, methodology, and level of detail. These samples help companies understand how a USPAP-compliant, audit-ready valuation report is prepared.